How To Calculate Your Commercial MACRS Solar Depreciation

When it comes to investing in solar energy systems for your business, understanding how to maximize your financial returns is just as important as the decision to invest in renewable energy solutions. One of the most powerful tools at your disposal is the Modified Accelerated Cost Recovery System (MACRS), a tax depreciation method that allows you to recover the cost of your solar assets more quickly through tax deductions.

This guide will walk you through the essential aspects of MACRS by providing a clear and concise overview of its key aspects outlined in IRS’s Publication 946 (2023), How To Depreciate Property. We’ll delve into the intricacies of calculating depreciation deductions, understanding recovery periods, and navigating the various depreciation methods available.

At ArtIn Energy, we’re here to help ensure your company takes full advantage of the tax benefits available. Our team can provide personalized guidance and assistance, helping you optimize your solar investment and maximize your tax savings.

Don’t hesitate to contact us to schedule a consultation and explore how MACRS can benefit your business on its journey to be powered by solar energy.

Key Takeaways

- MACRS is a powerful tool for maximizing tax benefits: By understanding and effectively using MACRS, businesses can significantly increase their return on investment in solar energy systems.

- The depreciable basis is crucial: The initial amount that will be depreciated is the depreciable basis, which is calculated based on the cost of the property, adjusted for applicable credits and deductions.

- MACRS offers multiple methods and recovery periods: The General Depreciation System (GDS) and the Alternative Depreciation System (ADS) provide different methods and recovery periods for calculating depreciation.

- ArtIn Energy can provide expert guidance: Our team of experts can assist you in navigating the complexities of MACRS and ensuring that you maximize your tax savings.

What is MACRS?

MACRS stands for Modified Accelerated Cost Recovery System. It’s a tax method used to calculate depreciation deductions for most business and investment property acquired after 1986. This system allows businesses to deduct a portion of the cost of their assets over a specific period.

The two primary systems within MACRS are the General Depreciation System (GDS) and the Alternative Depreciation System (ADS).

The GDS is generally the preferred method for most assets. It offers faster depreciation schedules, allowing businesses to deduct a larger portion of the asset’s cost in the earlier years of its useful life.

The GDS is typically used for solar energy systems with a recovery period of 5 years. This means that you can deduct a significant portion of the cost of your solar system over the first few years of ownership.

The ADS, on the other hand, provides slower depreciation schedules, resulting in smaller deductions over a longer period. It is typically used in situations where certain tax benefits or limitations apply.

MACRS offers various depreciation methods, such as straight-line, declining balance, and 150% declining balance. These methods determine how the cost of the asset is allocated over the recovery period.

Understanding the MACRS rules and selecting the appropriate depreciation method is crucial for maximizing tax savings for solar energy projects.

Tangible Property Eligible for Depreciation

To qualify for depreciation under MACRS, a solar energy system must meet the following criteria:

- Ownership: The company must own the solar panels, other clean energy products, and all associated equipment.

- Business Use: The solar system must be used to power the business’ operations or income-producing activities.

- Determinate Useful Life: The IRS has established a valuable life for solar panels, which is typically 5 years under the General Depreciation System (GDS).

- Tangible Asset: Solar panels are considered tangible property, meaning they have a physical form.

- Placed in Service: The system must be in service during the tax year you claim depreciation. This generally means the system is ready and available for its intended use.

- Capitalized Costs: All costs associated with the acquisition, installation, and preparation of the solar system for use must be capitalized and included in the depreciable basis.

Exceptions and Special Cases

Leased Property: You can only depreciate leased property if you retain the incidents of ownership. This means you bear the risk of loss or damage to the property and benefit from any appreciation in its value.

Property Types Excluded from MACRS Depreciation

These property types are excluded from MACRS:

- Pre-1987 Property: Property placed in service before 1987 is generally not subject to MACRS depreciation.

- Certain 1986 Property: Some specific types of property owned or used in 1986 may be excluded from MACRS.

- Intangible Property: Intangible assets, such as patents, copyrights, and goodwill, are generally not depreciated under MACRS.

- Nontaxable Transfers: Property acquired in a nontaxable transfer from a corporation or partnership may be subject to different depreciation rules.

Timing of Depreciation: Start and End Points

Property begins to depreciate when it is placed in service for use in its trade or business or for the production of income. This generally occurs when the property is ready for use and employed in a way that generates income or benefits the organization.

Depreciation continues until one of the following events occurs:

- Full Cost Recovery: The organization has fully recovered the cost or other basis of the property through depreciation deductions.

- Retirement from Service: The property is no longer used in the organization’s business or to generate income.

It’s important to note that the specific timing of depreciation may vary depending on the depreciation method and other factors.

Calculating the Depreciable Basis

The depreciable basis is the initial amount that will be depreciated over the recovery period. It represents the cost or other basis of the property, adjusted for any applicable tax credits or other factors.

Determining Initial Basis of Solar Property

The basis for depreciation of MACRS property is determined by the property’s cost or other basis, which is adjusted by the percentage of its use for business or investment purposes. Once this adjusted basis is calculated, it is further reduced by specific credits and deductions that apply to the property.

This means that to calculate the depreciation deduction, you must first determine the basis of the solar property. This typically includes the cost of acquiring the property, plus any installation costs or improvements made to the property.

Additional factors that may affect the basis include:

- Business or Investment Use: If the property is used for business and personal purposes, the basis must be adjusted to reflect the business use percentage.

- Section 179 Property: If the property qualifies for the Section 179 deduction, the depreciable basis is reduced by the amount of the deduction.

- Energy-Efficient Building Deductions: If the property qualifies for energy-efficient building deductions, the depreciable basis is increased by the amount of the deduction.

- Credits for Disabled Access and Employer-Provided Childcare Facilities: If the property qualifies for these credits, the depreciable basis is reduced by the amount of the credits.

- Special Depreciation Allowances: Certain property types may qualify for special depreciation allowances, which can affect the depreciable basis.

- Investment Credit Property: If the property qualifies for the investment tax credit, the depreciable basis is reduced by the credit amount.

Federal Solar Tax Credit (ITC) Impact

The IRA renewable energy’s Federal Solar Tax Credit (ITC) significantly reduces the cost of solar property. However, when calculating depreciation under MACRS, the depreciable basis of the solar property must be adjusted to account for the ITC.

- Basis Reduction: The depreciable basis is reduced by half of the ITC percentage. For example, if a business claims a 30% ITC, the depreciable basis is reduced by 15% before depreciation is calculated.

This adjustment lowers the total amount that can be depreciated, affecting the overall tax benefits derived from depreciation.

Impact of PTC vs. ITC

When choosing between commercial solar tax credits Production Tax Credit (PTC) and the Investment Tax Credit (ITC) for solar energy investments, it’s essential to consider how each impacts the depreciable basis.

- ITC: The ITC requires a reduction in the depreciable basis, which lowers the amount that can be depreciated.

- PTC: The PTC does not require any reduction in the depreciable basis. This means that you can depreciate the total cost of the solar property, potentially increasing your tax savings over time.

The ability to fully depreciate the property without adjustment under the PTC can be a significant factor in financial planning for solar investments.

Figuring the Depreciation Deduction Using MACRS

Once you’ve determined the depreciable basis, the next step is to calculate the annual depreciation amounts using the MACRS tables and methods.

Adjusting Basis for MACRS Depreciation

To calculate the depreciable basis for MACRS purposes, you must adjust the basis of the property for business or investment use and reduce it by any applicable credits and deductions.

Understanding Depreciation Systems (GDS vs. ADS)

The General Depreciation System (GDS) and the Alternative Depreciation System (ADS) are two different methods for calculating depreciation under MACRS. The system you use determines the depreciation method and recovery period for your property.

Recovery Periods Under GDS and ADS

The recovery period is the number of years over which you can deduct the cost of your property. The recovery period for solar energy property is typically 5 years under GDS. This means that you can deduct a significant portion of the cost of your solar system over the first few years of ownership.

Recovery period under GDS

| Property Class | Recovery Period |

| 3-year property | 3 years* |

| 5-year property | 5 years |

| 7-year property | 7 years |

| 10-year property | 10 years |

| 15-year property | 15 years** |

| 20-year property | 20 years |

| 25-year property | 25 years*** |

| Residential rental property | 27.5 years |

| Nonresidential real property | 39 years**** |

See the full table here.

Applicable Conventions for Depreciation

The convention you use determines when the recovery period begins and ends. There are three conventions:

- Half-Year Convention: This is the most common convention and assumes that the property is placed in service at the midpoint of the year.

- Mid-Quarter Convention: This convention is used if more than 40% of your property is placed in service during the last quarter of the year.

- Monthly Convention: This convention is used if more than 40% of your property is placed in service during the last month of the year.

Methods for Calculating Depreciation

MACRS provides three depreciation methods under GDS and one depreciation method under ADS:

- 200% Declining Balance Method: This method results in higher depreciation deductions in the early years of the recovery period.

- 150% Declining Balance Method: This method also results in higher depreciation deductions in the early years, but not as much as the 200% method.

- Straight Line Method: This method results in equal depreciation deductions over the entire recovery period.

How to Calculate Your Depreciation Deduction

To figure your depreciation deduction under MACRS, you first need to determine the following:

- Depreciation System: GDS or ADS

- Property Class: This determines the recovery period.

- Placed in Service Date: This determines the recovery period and convention.

- Basis Amount: The cost or other basis of the property, adjusted for any applicable credits or deductions.

- Recovery Period: The number of years over which you can deduct the cost of the property.

- Convention: The method used to determine when the recovery period begins and ends.

- Depreciation Method: The method used to calculate the annual depreciation deduction.

Once you have this information, you can calculate your depreciation deduction using either the IRS percentage tables or your own calculations.

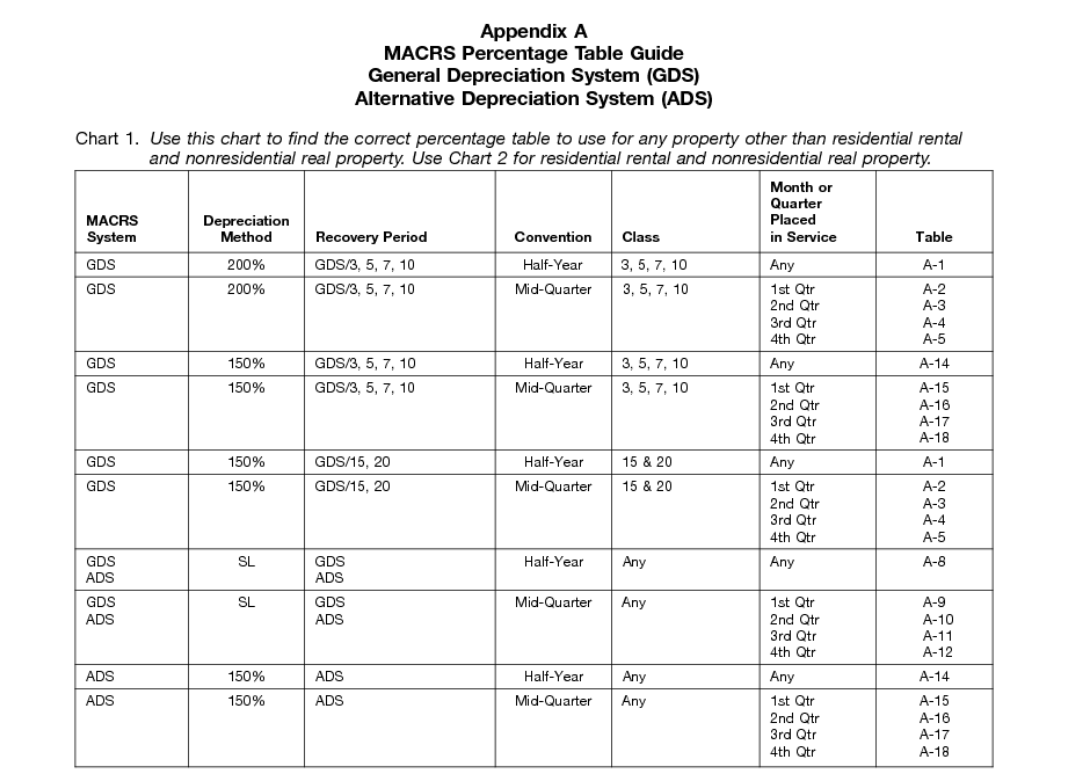

Using MACRS Percentage Tables

The IRS has established percentage tables that can help you figure your depreciation deduction under MACRS. These tables incorporate the applicable convention and depreciation method, making it easier to calculate your deductions.

The image shows MACRS Percentage Table 1, see other charts here.

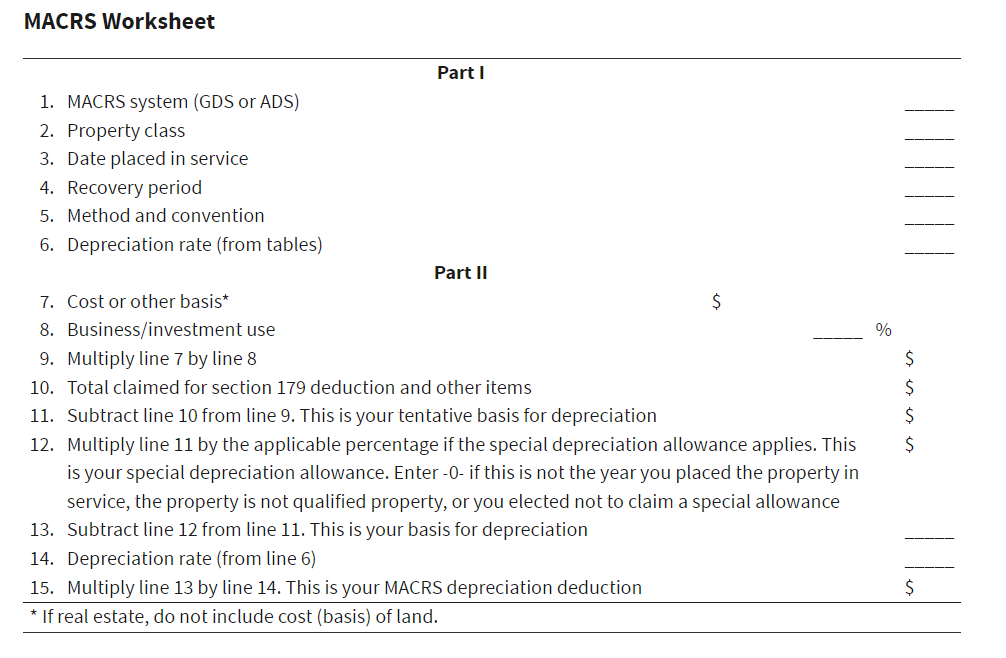

Using MACRS Worksheets

To further simplify the calculation process, you can use MACRS worksheets. These worksheets provide a step-by-step guide for figuring out your depreciation deduction using the percentage tables. Use a separate worksheet for each property item.

Calculating Depreciation the Tables

If you prefer to calculate depreciation manually without using the percentage tables, you can follow these steps:

- Reduce the adjusted basis: Subtract any depreciation claimed in previous years from the property’s adjusted basis.

- Apply the depreciation rate: Calculate the depreciation for the year using the declining balance method. The depreciation rate is determined by the depreciation method and the recovery period.

- Adjust for conventions: Adjust the depreciation amount based on the applicable convention (half-year, mid-quarter, or mid-month).

- Switch to straight-line method: Once the straight-line method results in a larger deduction than the declining balance method, switch to the straight-line method.

- Recalculate depreciation rate: For the straight-line method, recalculate the depreciation rate annually based on the remaining recovery period and applicable convention.

Remember that the timing and amount of your depreciation deductions will vary depending on the depreciation method, convention, and recovery period used.

Real-World Example of MACRS Depreciation

In this example, we’re calculating the depreciation for a solar energy system using the Modified Accelerated Cost Recovery System (MACRS) over a 6-year period.

Data & Methods

- Depreciation Method: General Depreciation System (GDS) using the 200% Declining Balance (DB) method.

- Initial Basis: The original cost of the solar property is $100,000.

- ITC Adjustment: The Federal Solar Tax Credit (ITC) reduces the basis by 15% of the initial cost ($15,000).

- Adjusted Basis: The basis after the ITC adjustment is $85,000.

- Depreciation Rate: The depreciation rates are based on the 200% DB method as per MACRS.

| Year | Depreciation Rate | Annual Depreciation Amount |

| 1 | 20% | $17,000 |

| 2 | 32% | $27,200 |

| 3 | 19.20% | $16,320 |

| 4 | 11.52% | $9,792 |

| 5 | 11.52% | $9,792 |

| 6 | 5.76% | $4,896 |

Mastering MACRS Depreciation for Your Solar Investment

Maximizing your tax benefits is essential for the success of any solar energy investment. By understanding and effectively utilizing MACRS, your company can significantly increase your solar IRR and ROI.

At ArtIn Energy, our team of expert renewable energy consultants can provide invaluable guidance and support throughout the entire process. From determining the most suitable depreciation method to ensuring accurate calculations, our team is dedicated to helping you maximize your tax savings.

Don’t miss out on the opportunity to optimize your solar investment and get the best of solar energy investment while contributing to a future powered by renewable energy sources. Contact us to schedule a consultation and explore how our expertise can benefit your business.